Financial Literacy: What Is It and Why Is It Important?

Oct 8, 2024 | 5 min. read

Many Americans lack basic financial knowledge. Develop the skills you need so you can manage your money and make smart financial decisions.

Your finances play a huge role in your life, impacting nearly everything you do, so having the knowledge to effectively manage your money is crucial. Financial literacy – or financial readiness, as it’s often called in the military – is your level of financial know-how. From managing this month’s budget to saving for your future retirement, good financial skills can make a significant difference in your family’s well-being in both the near and long term.

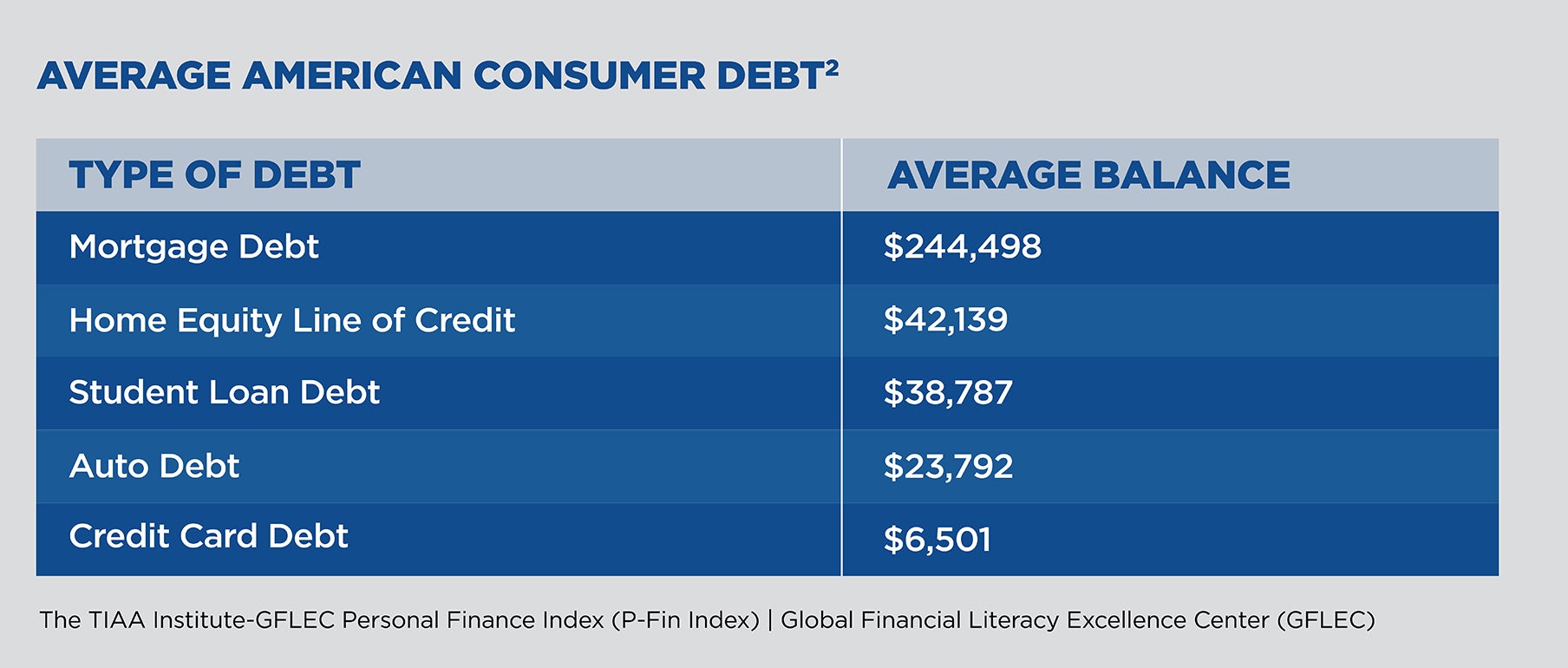

Data shows Americans aren’t as financially literate as we could be, though. The Personal Finance Index studies our understanding of financial topics like earning, saving, investing, debt and financial risk, and most U.S. adults can only answer about half of its financial quiz questions correctly.1 Additionally, consumer debt is at an all-time high, with the Federal Reserve reporting the average household carries a substantial amount of debt.

In this article, we’ll define financial literacy and introduce its fundamental components. We’ll also provide helpful resources so you can take intentional steps to increase your financial know-how and better equip your family to manage its money.

Key Takeaways

- Knowledge of money matters can empower military families to improve their financial circumstances.

- Your understanding of banking, budgeting, saving, investing, credit and debt determines your degree of financial literacy.

- Financial education combined with professional advice can result in saving more money and having greater financial confidence.

What is Financial Literacy?

Financial literacy is the ability to understand and use financial knowledge to manage the money you earn, spend, save, invest and borrow. It includes budgeting, managing credit and debt, and building wealth. If you are financially literate, you have and can apply the skills needed to fund today’s needs as you work toward tomorrow’s goals.

Financial Literacy in the Military

Military life presents unique challenges. Deployments, PCSing, spouse underemployment, and the hazards of the job can affect financial well-being, so acquiring money knowledge is important from the earliest days of your career.

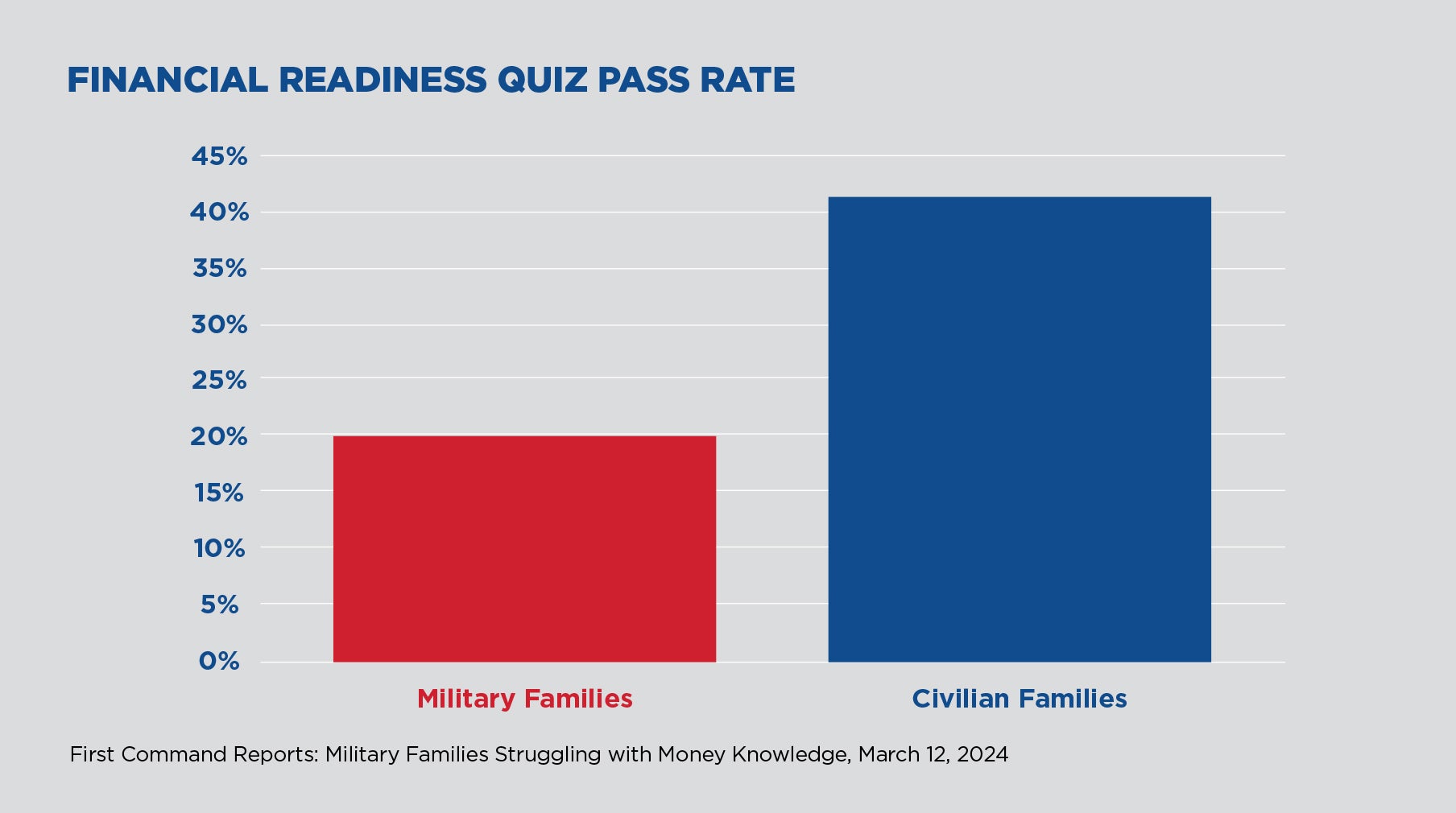

First Command’s 13th annual financial readiness test and survey, which measures financial understanding, revealed that middle-class military families are behind comparable civilian families in their knowledge of financial fundamentals. In fact, only 20 percent of military test takers passed the nine-question quiz, and the average score was just 59 percent.

A persistent trend also emerged. Military test takers scored lower than the general population in 11 out of 13 years, further highlighting the need to bolster financial literacy among service members and their spouses. To gauge your level of personal finance knowledge, try our nine-question financial readiness quiz.

Why is Financial Literacy Important?

Understanding finance fundamentals strengthens financial decision-making, helping you make good financial moves and avoid bad ones. In a complex financial landscape, it’s more important than ever to have the knowledge to effectively navigate it. Banking and credit options are expanding, so financial literacy can give you the skills to evaluate them and make advantageous choices. Longer term, responsibility for retirement planning has shifted to individuals since employer-managed pensions have dissipated. It’s now up to you to save and invest for retirement.

Even for military retirees who do (or will) earn a government-managed pension, financial know-how remains crucial. While you may be one of the few with a pension that’s managed for you, it’s just one part of your financial picture. You remain responsible for your Thrift Savings Plan (TSP) contributions and investment choices, non-government-sponsored savings and investments, banking tasks, and managing your credit and debt.

Benefits of Improving Your Financial Literacy

A higher level of financial literacy can benefit every decision you make that involves money, from budgeting and reducing debt, to saving money and growing wealth. Studies confirm the benefits of financial readiness. The Financial Industry Regulatory Authority (FINRA) is the body authorized by the U.S. Congress to protect America’s investors. In its National Financial Capability Study, FINRA found that respondents who scored above the median on its financial literacy quiz made better financial decisions than those with less financial knowledge.3 Financially literate individuals:

- Were more likely to make ends meet.

- Spent less of their income.

- Set aside money in an emergency fund.

- Were more likely to take steps for their long-term financial future.

A bonus benefit of financial literacy is a reduction in financial stress. When your finances are in good shape, peace of mind often follows.

Consequences of Financial Illiteracy

Conversely, what can result from inadequate financial knowledge? Essentially, it’s the opposite of the good financial behaviors just presented. The consequences can be high debt, the inability to live within your means, the lack of savings for life’s inevitable emergencies, failing to save, invest or prepare for your future, and – financial stress. Without a doubt, the inability to adequately provide for your family can be a profound stressor.

What Fundamental Knowledge Is Needed for Financial Literacy?

To be financially literate, you need to understand the fundamentals of banking, budgeting, saving, investing, credit and debt.

Banking

A bank account – usually the starting point of your financial journey – is where you store your money and where it can begin to earn interest and grow. It’s often required for other financial endeavors like using a debit or credit card, using payment apps like Zelle®, writing checks, using an automated teller machine (ATM), buying or renting a home, and receiving payments from an employer.

Competing banks offer many of the same types of accounts – like savings, checking, and high-yield savings – but they can differ in their services, fees, interest rates, deposit requirements, and accessibility. Knowledge of the alternatives will help you determine which is right for you.

Budgeting

A budget is your day-to-day tool for managing your money. It enables you to track your expenses against your income to avoid spending more than you earn. By using a budget to keep spending at a level that is less than your income, you can not only avoid the trap of high-interest debt, but also allocate the money left over every month to other important financial objectives, like reducing debt, saving and investing.

Saving

Saving money is the process of setting aside cash in a safe, accessible account, and your deposits usually earn interest. How much you should save varies based upon your needs, lifestyle and income. A skilled financial advisor can help you review your circumstances to set a goal that’s right for you.

An emergency fund is an important type of savings account that serves as a cushion to get your family through unexpected financial challenges without incurring debt. In most cases, it is built over time, and saving enough to cover three to six months of expenses is commonly recommended. Because of the stability of employment and income in the military, an amount equal to two to three months of expenses may be sufficient for your family.

Investing

Investing is the process of buying an asset with the hope that it will increase in value or generate income. In the context of financial planning, investing is typically done as part of an effort to build wealth and pursue specific goals over time. It often involves purchasing financial securities like stocks, bonds, treasuries and mutual funds. Real estate, precious metals and collectables are other forms of investment.

Setting realistic financial goals, determining how much to invest, choosing specific investments, and determining how to allocate your funds across those investments based on your time horizon and tolerance for risk all represent some of the challenging decisions that require significant financial know-how. A knowledgeable professional can help, especially a fiduciary financial advisor, who is legally required to put your best interests ahead of their own.

Credit

Credit is the concept of getting something now and paying for it later. It most often involves borrowing money or accepting items like groceries or a car, with the commitment to repay the loan or pay for the goods over time – usually with interest. Some of the most common forms of credit are car loans, home loans, student loans and credit cards.

Your credit score is a number that rates how credit worthy you are, and it’s based on your credit repayment history. This score is used by lenders to determine whether you will be approved for future loans or credit, how much you’re eligible to receive, and the interest rate you’ll be charged as you repay it. It’s important to responsibly manage your credit and build a good credit score so that once you’re ready for a significant financial move, like buying a car or a house, you can qualify for credit at favorable terms.

No discussion of credit is complete without a look at credit cards. Issued by banks that serve as your lender, credit cards allow you to easily purchase items on credit. Your bank pays the seller in full while you repay the bank over time – and as mentioned previously, often with interest. A credit card is a convenient tool for making purchases without cash and using one can help build your credit score. But, it can also make it tempting to overspend and accumulate unwanted, high-interest-rate debt. Smart credit card users pay their account balance in full each month to avoid interest charges, which only add to the cost of purchases and decrease the money available for other financial goals. Numerous credit cards exist with wide-ranging features. Gaining financial intelligence can help you select one that’s well-suited to your needs, so you can use it to your advantage.

Debt

Debt is money borrowed from a lender that the borrower agrees to repay, usually with interest. It’s smart to avoid unnecessary debt, but it isn’t always feasible to pay cash for high-cost items like a home, car or college education. In certain circumstances, debt can be the right choice if it helps you accomplish a positive, longer-term financial outcome. A home mortgage can allow you to build ownership equity and recoup housing costs when you sell. A reasonable car loan can allow you to commute to your job to earn income. But too much debt, especially at high interest rates, can become burdensome, resulting in late payments, extra fees, interest charges, and a lower credit score. Financial knowledge can help you make smart debt management decisions about the expenses that justify debt, the lenders and terms to accept, the total amount of debt to carry, and the best strategy to pay debt down.

How Do You Improve Your Financially Literacy?

As with any unfamiliar topic, you increase your knowledge by taking purposeful steps to learn more about it. To enhance your financial skillset, take advantage of these resources:

- Federal Reserve Education offers podcast, articles, videos and webinars.

- The FINRA Foundation helps Americans build financial stability, invest for life goals, and guard against fraud. Its programs address the needs of investors, including military service members.

- The Department of Defense Office of Financial Readiness oversees efforts to help military families achieve personal financial readiness as an integral component of mission readiness. Check with your unit for additional financial readiness resources.

- MyMoney.gov compiles federal government resources designed to strengthen Americans’ financial capability.

- The First Command Education Foundation is a non-profit organization dedicated to improving financial readiness, especially for those who serve in the military. Its educational programs provide information to improve the skills needed to make intelligent financial decisions and include resources on military financial readiness.

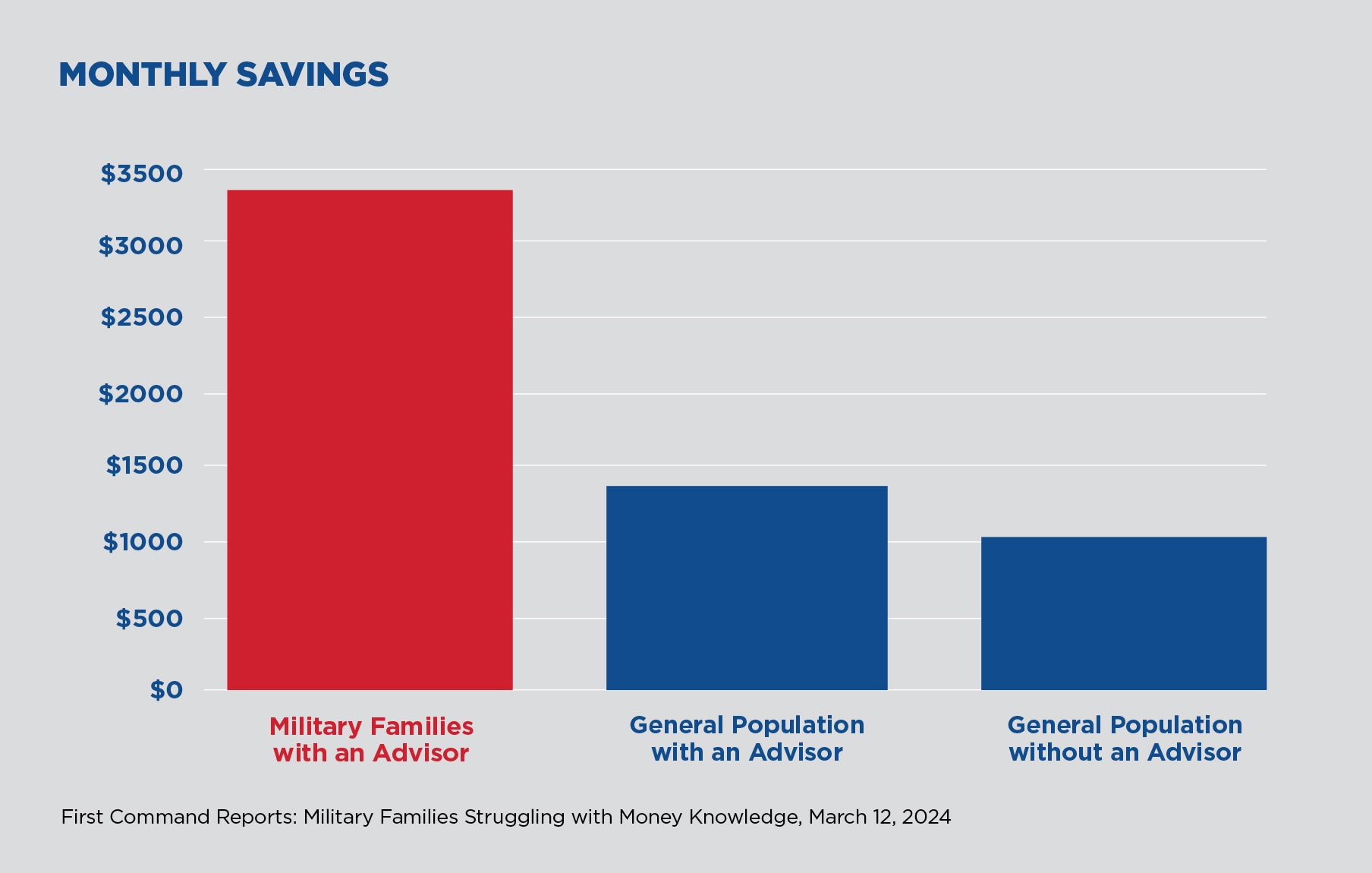

Financial education is a critical first step but isn’t always sufficient on its own. After all, you have a family, career and other priorities that compete for your time. Another resource you can leverage is the support of a knowledgeable financial advisor. First Command’s research shows military families that work with an advisor report saving more and having a greater level of financial confidence than those in the general population.4 In fact, military families with an advisor save more than twice as much as general population families with an advisor and over three times more than those who don’t have an advisor.

Coaching clients on positive financial behaviors is an important and intentional approach we take, and we’re dedicated to helping clients increase their knowledge as they pursue financial well-being. The combination of good financial skills and a partnership with a trusted advisor can help put your family on the path to financial security.

1The TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) | Global Financial Literacy Excellence Center (GFLEC)

2Average American Debt : Household Debt Statistics (businessinsider.com)

3National Study by FINRA Foundation Finds U.S. Adults’ Financial Capability Has Generally Grown Despite Pandemic Disruption | FINRA.org

4First Command Financial Behaviors Index®

TSP funds have very low administrative and investment expenses and, low expenses can have a positive effect on the rate of return of your investment.

Get Squared Away®

Let’s start with your financial plan.

Answer just a few simple questions and — If we determine that you can benefit from working with us — we’ll put you in touch with a First Command Advisor to create your personalized financial plan. There’s no obligation, and no cost for active duty military service members and their immediate families.