Social Security Fairness Act (SSFA) News: What It Means for Your Retirement

Apr 10, 2025 | 4 min. read

Update: How the SSFA/HR 82 can impact your Social Security benefit, retirement income, and financial future.

What is the Social Security Fairness Act?

The SSFA is a new law that will increase the Social Security benefit of approximately 3.2 million Americans. The act repeals the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), two provisions from the late 70s and early 80s that unfairly reduced Social Security benefits for certain public-sector employees and their spouses.

When was the Social Security Fairness Act signed into law and when does it take effect?

The act took effect when it was signed into law on Jan. 5, 2025. Adjustments to benefits for impacted individuals already drawing Social Security are retroactive to January of 2024. For those who haven’t yet claimed Social Security, the SSFA will be factored into the calculation of their benefit on their filing date.

The Social Security Administration’s (SSA) implementation is of the SSFA is progressing rapidly and is ahead of the schedule that was initially projected. The agency expected to complete the processing of one-time retroactive payments as well as adjustments to future benefit payments by the end of March 2025, with deposits to on-file accounts occurring in April. For complex cases that can’t be processed automatically, retroactive payments and new monthly benefit amounts must be handled manually and may require extra time. The SSA recommends waiting until after April deposits are issued before making inquiries.

Who is affected by the Social Security Fairness Act?

Only people who receive a pension based on work not covered by Social Security and earned Social Security benefits in a covered job may see benefit increases. This includes many public-sector employees, including teachers, firefighters, police officers, and other government workers, as well as beneficiary spouses. Some of these roles are non-covered, meaning they aren’t covered by Social Security. Workers do not pay Social Security taxes on their wages and are not eligible to draw Social Security based on them in retirement. These public-sector workers are not covered by Social Security because they are eligible for government pensions. To prevent the collection of both a pension and Social Security based on these non-covered jobs, the WEP and GPO provisions were enacted.

Unfortunately, the WEP and GPO prompted an inequity for some, specifically those who, in addition to their non-covered public-sector jobs, also held jobs during their working years that were covered by Social Security and for which they did pay Social Security taxes. WEP and GPO unfairly reduced or eliminated Social Security benefits for these workers, as well as their spouses, surviving spouses, and eligible former spouses. The passage of the SSFA corrects this issue by restoring full Social Security benefits for those impacted by the WEP or GPO. This includes retired and current public-sector employees, spouses, surviving spouses, and in certain cases, former spouses, who are eligible for a government pension as well as Social Security benefits from other covered work. Not all public-sector workers, retirees or spouses will see an adjustment in their Social Security benefit.

What do impacted individuals need to do?

If your Social Security benefit is currently reduced by WEP, or if you are a spouse, surviving spouse, or former spouse whose benefit is affected by GPO, it’s important to verify your mailing address and direct deposit information with the SSA. Usually, the best way to check it is by visiting www.ssa.gov/myaccount. As implementation of the SSFA proceeds, SSA officials will calculate and adjust your monthly benefit and issue a payment to cover benefit increases retroactive to January of 2024.

Workers and spouses who have not yet applied for Social Security benefits because of WEP or GPO may need to file an application. Keep in mind that all other Social Security laws and policies – like benefit reductions for claiming before the full retirement age – still apply. Because everyone’s financial circumstances differ, the right time to file for Social Security varies. Working with a financial advisor can help you determine the timing that’s optimal for you.

For new applicants, the SSA recommends applying at www.ssa.gov/apply, however the survivor benefit application is not available online. SSA representatives will take applications by phone for surviving spouses and those who have not previously applied for retirement benefits due to WEP or GPO.

For more information on the SSFA and updates on its implementation, visit the SSA’s website.

Does the Social Security Fairness Act impact members of the military?

Passage of the SSFA does not affect military benefits, like the pension a retired veteran can receive. However, the Social Security benefit of military veterans and their spouses can be affected by the act. Since military service is covered by Social Security, and has been since 1957, service members pay taxes into the system on their active-duty military base pay and are entitled to draw Social Security income based on it in retirement. But, like other public-sector workers in non-covered jobs, if a service member also held a non-covered job during their working years and draws a pension for it, the Social Security benefit of retired service members, spouses or surviving spouses based upon their military income may have been reduced because of WEP or GPO. The SSFA’s repeal of these provisions means such reductions no longer apply.

Does the Social Security Fairness Act impact my taxes?

A portion of Social Security benefits are taxable depending upon a taxpayer’s income and filing status. If your Social Security benefit increases because of the SSFA, it may affect your taxes. Additionally, retroactive payments dating back to January of 2024 that result from the SSFA will be issued as a lump sum and are considered taxable income for the year in which they are received. So, receiving a lump-sum payment in 2025 increases your taxable income for that year, which potentially affects your tax liability and Medicare premiums. It’s advisable to consult with a qualified tax professional to understand how a lump-sum payment may impact your specific tax situation. Visit the IRS website for more information on the taxation of Social Security benefits.

Does the Social Security Fairness Act impact your financial plan?

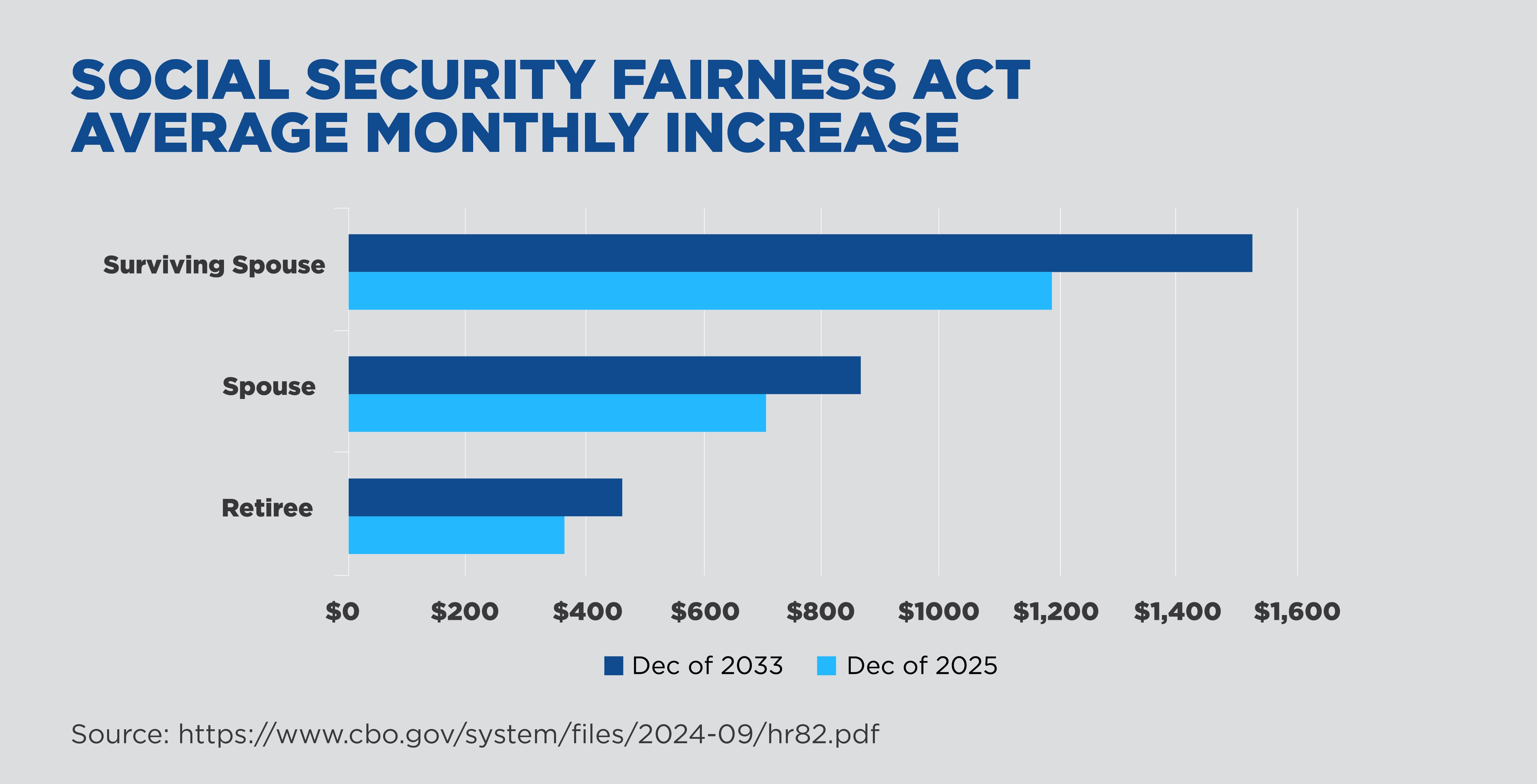

The SSFA can have a substantial impact on your financial plan and retirement income. The Congressional Budget Office (CBO) estimates that retirees affected by WEP will see an average monthly benefit increase of $360 for December of 2025, increasing to $460 over the next eight years. The CBO reports spouses affected by GPO will see an average monthly increase of $700 in December of 2025 and surviving spouses will see an average monthly increase of $1,190. Eight years later, the average monthly benefit will grow to $860 for spouses and $1,520 for surviving spouses.

An increase in your Social Security benefit from the SSFA can bolster your financial picture by providing additional resources in retirement, so it's essential to evaluate its impact on your finances. You’ll want to consider how a benefit increase can be utilized and then update your long-term financial plan if you have one.

Your Financial Advisor can help you make the most of an increase in your Social Security benefit.

Navigating the changes brought about by the SSFA can be complex, highlighting the importance of working with a knowledgeable financial advisor who can help you understand the impact of the new law on your Social Security benefit and overall financial picture. Through personalized advice that’s tailored to your circumstances, your Advisor can help you make smart decisions about the increased role Social Security may play in your retirement income and when to claim your benefit. Reach out to your Financial Advisor or get started with one today.

First Command does not provide legal or tax advice, and this article does not contain any legal or tax advice. Any recommendations provided to you in this article are strictly for financial planning purposes only. Should you require legal or tax advice, you should consult with your attorney or tax advisor.

Get Squared Away®

Let’s start with your financial plan.

Answer just a few simple questions and — If we determine that you can benefit from working with us — we’ll put you in touch with a First Command Advisor to create your personalized financial plan. There’s no obligation, and no cost for active duty military service members and their immediate families.